home

about

our services

our process

our team

our locations

INSIGHTS

client login

Case Studies

careers

get started

"This is a quote from a Coyle Leader. These can appear randomly from a few select quotes."

We all experience instinctual reactions when presented with risk, ranging from “avoid at all costs” to “let’s go for it!” For most of us, we have learned to take a measured approach when presented with risks as well as opportunities in our lives. We understand that many risks can be managed through prudent planning, while others need to be assumed rather than avoided in pursuit of our long-term goals and aspirations.

Life is a constant dance with risk. It is everywhere and ever present. We are forever trying to tame it, eliminate it, or ignore it altogether. To mitigate some of our risks, we try to introduce some element of control: exercise regularly, watch what we eat, and get regular health checkups. We habitually lock our doors, install fire alarms, use sunscreen, get flu shots, and refill our prescriptions. We keep our vehicles and homes in good running condition, use seatbelts and wear bike helmets, use passwords and anti-malware software, and hire attorneys when needed.

To protect ourselves from financial risk, we purchase insurance policies that cover automobile accidents, property damage from tornadoes, floods, or fires, and catastrophic health emergencies. We purchase life insurance to protect our families from the risk of our “premature mortality.”

Broadly defined, risk is the possibility of an unwanted, adverse outcome. To no one’s surprise, investors also face a myriad of risks. One graduate-level investment textbook lists twenty different types of risks investors should consider when investing in stocks and bonds [1]

For stock investors, this includes firm-specific (or idiosyncratic) risk (the risk that an individual company you own shares in will underperform or fail). Another risk for equity investors is market risk (the everyday price movement of the whole stock market associated with macroeconomic developments such as interest rate changes, economic downturns, or recessions, or market-moving news such as COVID lockdowns or tariff announcements).

Fixed-income investors face other risks, among them interest rate risk (the risk of bond price changes due to changes in the general level of interest rates) and credit (or default) risk (the risk that the bond issuer will fail to repay the interest and/or principal when it’s due). We could add reinvestment risk, currency risk, and inflation risk here too, but you get the idea (plus I’m trying to keep this to 900 words or less).

There are several ways to think about investment risk. An early pioneer in studying the theoretical side of risk was Harry Markowitz, who published an important article in 1952 entitled “Portfolio Selection.” His insights formed the basis for portfolio theory and the importance of diversification.

Markowitz defined risk as the variance of asset prices (also known as volatility), a statistical measure of how widely the returns on an asset swing around their average. Individual stock investments, for example, have very high variances of returns (volatility) because of firm-specific risk. The price of a share of a company’s stock can fluctuate wildly. [2] Because firm-specific risk is unique to each company, no two stocks will vary in price in exactly the same way. This leads to an important insight from Dr. Markowitz: as you add more individual stocks to your portfolio, the volatility of the overall portfolio will be less than the average volatility of its individual holdings.

Thus, a well-diversified portfolio can effectively eliminate the firm-specific risk of the constituent stocks [3] This is a key insight of Markowitz’s work and gives rise to the important idea that portfolio diversification is a “free lunch” for investors. In other words, you gain exposure to weighted-average expected returns from each stock, but with less overall risk (volatility).

While I don’t know any clients who routinely think of investment risk in terms of a statistical concept like variance or standard deviation of returns, most investors are keenly aware of price volatility in their portfolios. They are especially displeased with downside volatility (and usually happy on the upside).

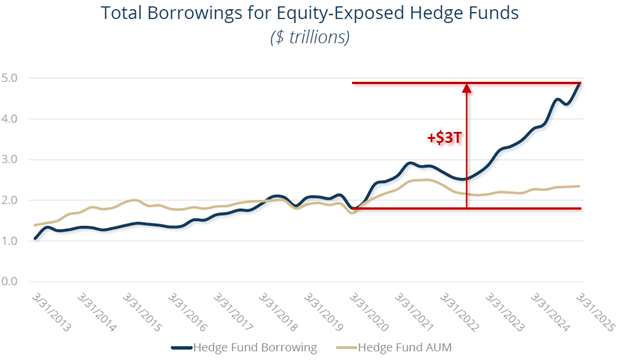

According to one of our managers, there is evidence that the equity markets this year have become increasingly volatile, as large, leveraged traders (using borrowed money to increase the size of their positions) have influenced the markets. For example, the following chart shows how equity-exposed hedge funds have increased their borrowings since 2020 by $3 trillion [4]:

It’s worth noting that not all investors worry about volatility. As Peter Bernstein writes in his excellent book Against the Gods: The Remarkable Story of Risk, “Even though risk means that more things can happen than will happen—a definition that captures the idea of volatility—that statement specifies no time dimension. Once we introduce the element of time, the linkage between risk and volatility begins to diminish… For true long-term investors, volatility represents opportunity rather than risk.”

We conclude by acknowledging that the statistical concept of variance of returns is a handy concept for use in academic formulas and theoretical models. But we must ask ourselves: is it the best proxy for risk for everyday investors?

One of our managers disagrees, saying, “Volatility is not risk… many investors are unwittingly focused more on avoiding volatility than protecting capital.” (Protecting capital means growing the asset over time at or in excess of the level of inflation.)

He goes on to say that investors should adjust their exposure to equity volatility based on two factors: (1) their spending needs, by matching the cash needed with investment cash flows and liquidity, and (2) their emotional tolerance for downside market volatility. [5]

We agree wholeheartedly. At Coyle Financial, our advisors are focused on helping our clients manage the risks associated with the pursuit of their financial objectives. For most of us, volatility is a reality that needs to be embraced in pursuit of the opportunity to achieve the long-term returns associated with investing in equities. The establishment of a long-term plan, supported by a structure of coordinated decision-making, is critical in building the confidence to stay the course when the next market downturn occurs.

[1] Bodie, Kane & Marcus, Investments, 11th Edition, McGraw Hill

[2] You can get a sense for this by looking at the price gap size in the 12-month high-low prices for any publicly traded stock.

[3] Of course, if you add enough stocks to your portfolio, you could end up owning the market portfolio, but you are still left with market risk.

[4] Used with permission from Clifford Capital Partners. LLC.

[5]“Capital Protection and Volatility”, Nick Sampras, ACR Alpine Capital Research LLC, July, 2025.

All information is from sources deemed reliable, but no warranty is made to its accuracy or completeness. This material is being provided for informational or educational purposes only, and does not take into account the investment objectives or financial situation of any client or prospective client. The information is not intended as investment advice, and is not a recommendation to buy, sell, or invest in any particular investment or market segment. Those seeking information regarding their particular investment needs should contact a financial professional. Coyle, our employees, or our clients, may or may not be invested in any individual securities or market segments discussed in this material. The opinions expressed were current as of the date of posting but are subject to change without notice due to market, political, or economic conditions. All investments involve risk, including loss of principal. Past performance is not a guarantee of future results.

Copyright © 2023 Coyle Financial Counsel. All rights reserved.

Start the conversation today by reaching out to our team.